Labor Market Weakness and Its Influence on the Housing Market

The weakening labor market has important implications for borrowing costs, which directly affect Florida’s real estate affordability. The Federal Reserve operates under a dual mandate of maximum employment and price stability. When unemployment rises as it has in Florida and nationally it signals softening demand and risks to the employment side of that mandate. In response, the Fed often cuts (No rate cut in April) the federal funds rate to make borrowing cheaper for businesses and households, encouraging spending, hiring, and economic activity.

This is why many economists and market participants expect that continued labor market softening could prompt modest rate cuts later in 2026, potentially easing 30-year mortgage rates from their current mid-6% range. In short, bad news on jobs can eventually become good news for mortgage rates though the timing and magnitude depend on how quickly inflation remains under control.

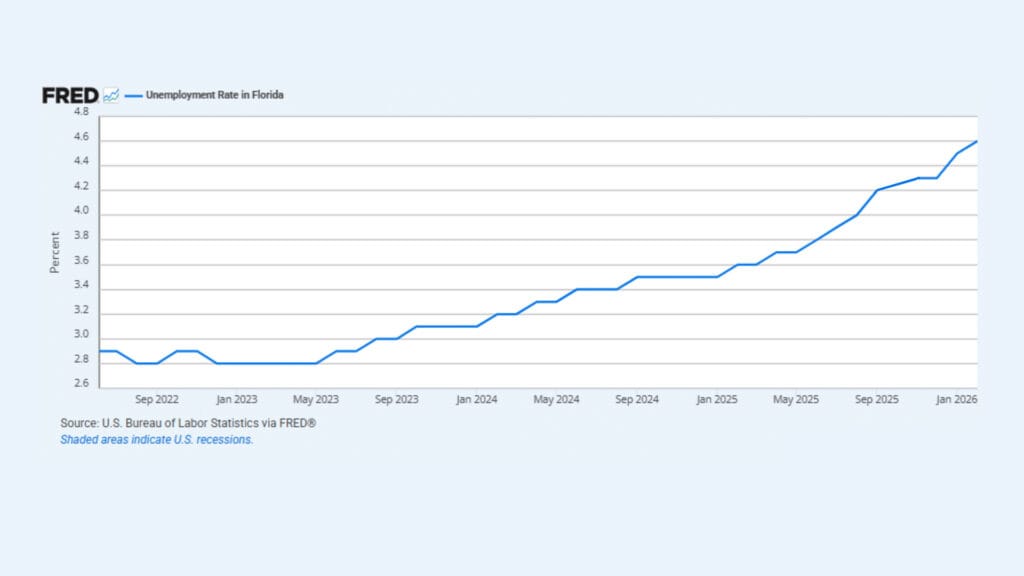

FLORIDA’S UNEMPLOYMENT RATE: A KEY CHART TO WATCH

Building on that Fed context, one of the most important charts for assessing Florida’s real estate health right now is the state’s unemployment rate from the U.S. Bureau of Labor Statistics (via FRED). After hovering at historically low levels around 2.8% in 2022-2023, the rate has climbed steadily and accelerated into 2025, now sitting at 4.6% as of February 2026.

Why does this matter for housing? A weakening labor market directly impacts buyer demand. Fewer employed households with stable incomes means slower mortgage approvals, less urgency to buy (or sell and relocate), and potential upward pressure on inventory as distressed sales rise. In Florida’s post-pandemic boom market, this shift comes after years of strong job growth that fueled migration and price appreciation. That said, if employment rebounds, more people gain the income stability to enter the market families move for better opportunities, retirees flock to affordable coastal areas, and investors spot rental potential in growing job hubs.

To get a fuller picture, let’s look at the Job Openings and Labor Turnover Survey (JOLTS) from the BLS. As of late 2025, Florida’s job openings remain elevated at around 500,000 statewide down from pandemic highs but still signaling demand for workers in key sectors. This mismatch (high openings amid rising unemployment) could indicate skills gaps rather than a full downturn, which is somewhat positive for real estate. For instance, if openings in healthcare and tech persist, it might attract more skilled migrants to areas like Miami’s tech corridor, supporting steady housing demand. Keep an eye on JOLTS updates via FRED; if openings drop sharply, it could amplify Fed rate cuts and make homes more affordable.

JOB GROWTH PROJECTIONS AND RIPPLE EFFECTS ON HOUSING PRICES

Despite the unemployment uptick, Florida’s economy remains a powerhouse, with 2026 projections suggesting continued momentum. The Florida Department of Economic Opportunity forecasts that nonfarm employment could reach approximately 10.2 million jobs by 2026, up from about 9.5 million in 2023 a growth rate of around 7% over three years. This expansion, driven by sectors like healthcare and professional services, is likely to fuel housing price increases, especially in high-demand metro areas. According to BLS and state forecasts, Florida’s labor force is expected to grow by about 1-1.5% annually, translating to heightened demand in robust job markets.

Rising incomes add another layer. With projected average wage growth of 3-4% annually through 2026 (per BLS estimates), more Floridians could enter the housing market. However, affordability isn’t always straightforward. In cities like Miami, where tech and finance jobs are booming, median home prices are forecasted to hit 550,00 by 2026 (based on Zillow’s long-term models), up from 450,000 in 2023. High-paying jobs attract affluent buyers, creating competition and bidding wars.

For first-time buyers or families, this means tighter affordability. Take Jacksonville, a logistics and military hub where job growth in transportation is projected at 2.5% by 2026. This could push median rents to $1,800 monthly, making homeownership a smarter long-term play if interest rates stabilize around 5-6% as predicted by the Federal Reserve.

MIGRATION PATTERNS TIED TO EMPLOYMENT

Florida’s appeal as a no-income-tax state draws remote workers and retirees, but labor market strength amplifies this. Projections from the University of Florida’s Bureau of Economic and Business Research indicate net migration could add 300,000 residents annually by 2026, many chasing jobs in healthcare (expected to grow by 12% statewide) and renewable energy sectors.

This influx strains housing supply. In Orlando, where tourism and tech converge, new job creation could lead to a 10% increase in home sales volume by 2026, per Redfin forecasts. Investors might find opportunities in multifamily rentals, as young professionals seek affordable options near employment centers like Lake Nona’s medical city.

THE IMPACT ON SELLERS, INVENTORY, AND RETIREES

Higher unemployment often means more homes on the market as people relocate for work or downsize. In areas like the Panhandle, where agriculture and military bases dominate, a dip in job stability could increase inventory by 15% by 2026, stabilizing prices and giving buyers more negotiating power. Sellers in these scenarios might need to price competitively or invest in updates to stand out.

For retirees, who make up a significant portion of Florida’s market, labor trends matter less directly but influence overall economic health. A stable job market supports tourism dollars, keeping property values strong in places like Naples or Sarasota.

SUMMARY

The Federal Reserve’s latest FOMC meeting on April 28–29, 2026, delivered no relief on rates. The central bank once again held the federal funds rate steady in the 3.5%–3.75% range, with markets assigning virtually zero chance of a cut. For Floridians already feeling the sting of a rising unemployment rate (now at 4.6% as of February 2026, up a full percentage point from a year ago), this decision adds another layer of pressure. Higher-for-longer borrowing costs will make mortgages more expensive at a time when job security is weakening, potentially delaying home purchases, cooling buyer demand, and leaving many families and first-time buyers on the sidelines. While Florida’s long-term fundamentals job growth in key sectors, continued migration, and no state income tax remain supportive, the combination of softening labor conditions and sticky interest rates means the housing market will likely face a challenging few quarters ahead for sellers.

ABOUT AUTHOR

Jaden Duxfield is a skilled Market Research Analyst at Sunland Group who brings a unique combination of strategic thinking and analytical expertise to the real estate industry. With a background in mechanical engineering and a degree from Auckland University of Technology, New Zealand, he offers a sharp understanding of the built environment. Jaden specializes in data-driven analysis to uncover emerging trends and guide investors and developers in making informed decisions. His proficiency in advanced statistics and Python programming is highlighted in his insightful blogs, where he transforms complex data into clear and actionable conclusions for industry professionals.

The information provided on this blog is for general informational purposes only and does not constitute financial, investment, or real estate advice. While I strive to present accurate and up-to-date information, the content may not reflect the latest market conditions or legal developments. Any reliance you place on such information is strictly at your own risk. Sunland Group and I do not make any representations or warranties regarding the accuracy, reliability, or completeness of the information provided.

Before making any financial or investment decisions, you should consult with a qualified professional who can provide advice tailored to your individual circumstances. Sunland Group and I will not be held liable for any losses or damages arising from the use of this blog or its content.

Blog

Explore our property blog for in-depth insights into residential and commercial market trends, lifestyle inspiration, expert advice and global real estate updates.

SUNLAND MARKET RESEARCH

Lehigh Acres: Prime time to buy and build your dream home

SUNLAND MARKET RESEARCH

The Crown Jewel of South West Florida

SUNLAND MARKET RESEARCH

Miami’s Waterfront Gems: Single-Family Homes Riding High Amid Migration Madness

CORPORATE OFFICE

14 NE 1st Ave, Suite 305,

Miami FL 33132

PHONE NUMBER

(305) 209 1455