Mortgage Rates Reach Yearly Low: A Potential Catalyst for Miami’s Sluggish Market

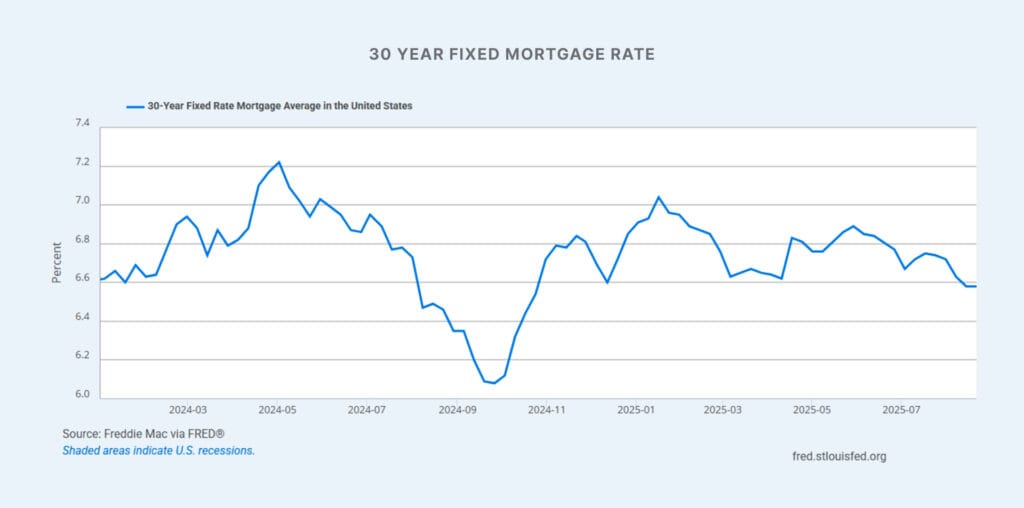

Mortgage rates for 30-year fixed loans have stabilized at 6.58%, their lowest point this year, providing a glimmer of relief amid broader economic pressures, as reported by Freddie Mac in their latest survey.

In this analysis, we’ll break down the interplay between these lower rates, building permits, market sentiment, and their influence on demand, with a focus on Miami’s single-family home sector. Drawing from recent data by the National Association of Realtors (NAR), Florida Realtors, and local market reports, we’ll examine how these factors signal a market slowdown and the potential for rate-driven recovery. Using our Miami Market Insight Framework, which integrates permit trends, sentiment indices, and rate-demand correlations, this piece highlights data-backed opportunities for investors and enthusiasts.

To understand the Miami market’s current state, we’ll segment the analysis into four core metrics: mortgage rates, building permits, market sentiment, and their collective impact on demand for single-family homes. Each is supported by quantitative data from authoritative sources.

MORTGAGE RATES AT A YEARLY LOW

Rates on 30-year fixed mortgages held steady at 6.58% in the most recent week, unchanged from the prior period, while 15-year rates edged down slightly to 5.69% from 5.71%, according to Freddie Mac’s Primary Mortgage Market Survey. This marks the lowest average for 30-year rates in 2025, down from a July average of 6.72% as cited by NAR. In contrast to mainstream optimism about rapid declines, this stabilization, while positive, remains elevated compared to pre-2022 levels, where rates hovered below 3%. Florida Realtors data further shows that stronger credit scores can reduce effective borrowing costs by enabling access to these lower rates, with payment history and credit utilization as key factors in securing savings of roughly 0.5% or more on interest.

BUILDING PERMITS: A POTENTIAL LEADING INDICATOR

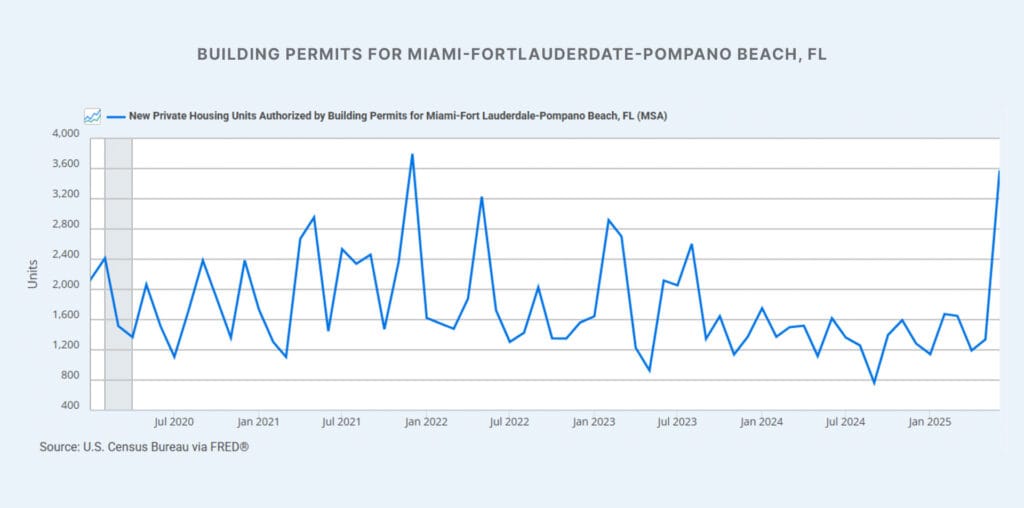

Building permits in Miami reflect a complex picture of developer activity amid evolving market conditions. Recent data indicates a significant uptick, with new private housing units authorized in the Miami-Fort Lauderdale-Pompano Beach MSA surging to 3,000+ units in June 2025, as shown in updated U.S. Census Bureau figures.. This contrasts with earlier reports of a 15% year-over-year decline in single-family home permits in the first half of 2025, suggesting a potential rebound. New home mortgage applications have also risen, driven by lower interest rates and increased inventory. Nationally, inventory stands at 4.6 months’ supply, per NAR, yet Miami’s recent permit surge could signal a leading indicator of renewed construction activity, challenging the notion of permits as merely a lagging metric. Additionally, home builders listed on the S&P 500 have reached yearly highs, which may indicate a shift in sentiment toward optimism, potentially driven by anticipated demand and improving market conditions, though sustained growth is needed to confirm this trend.

BUILDERS SENTIMENT

Builder confidence remains subdued, with the NAHB/Wells Fargo Housing Market Index dipping to 32 in August 2025, down one point from July and marking 16 consecutive months below the neutral threshold of 50, according to the National Association of Home Builders (NAHB). In Miami, prospective buyer traffic scored a low 22 on the index, up only marginally from prior months. Florida Realtors note a 7% month-over-month increase in new home applications in July, yet overall sentiment is weighed down by supply-side challenges, including regulatory hurdles for land development. This contrasts with the permit uptick and S&P 500 builder highs, suggesting a disconnect. NAHB Chief Economist Robert Dietz emphasizes that without further rate reductions, sentiment may stay low, hindering recovery, though the recent market indicators could hint at emerging optimism if conditions improve.

INFLUENCE ON DEMAND FOR SINGLE-FAMILY HOMES

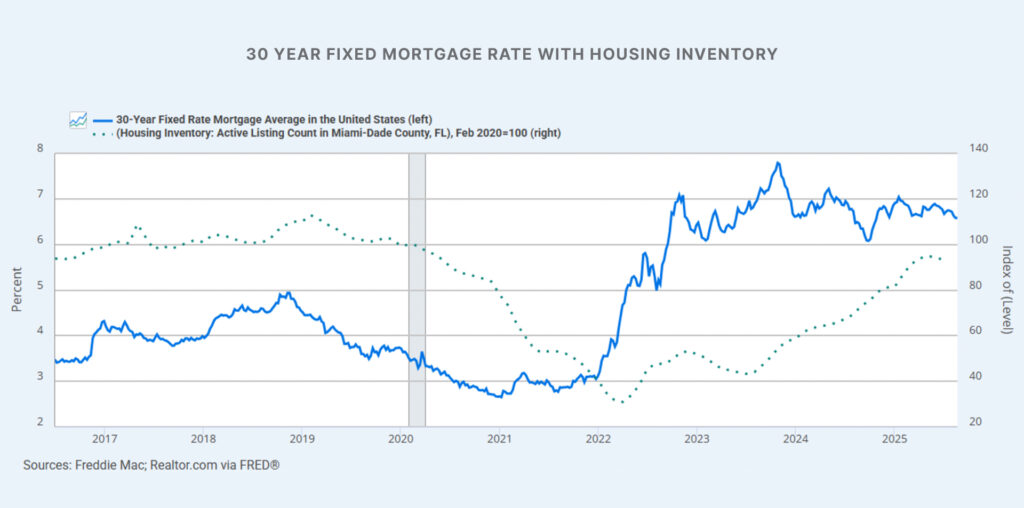

When we plot the 30-year mortgage rate, the most typical form of financing, with the active inventory in Miami-Dade County, we can see how interest rates are a leading indicator. Lower rates directly correlate with heightened demand, particularly in Miami’s single-family segment, where affordability is a key barrier. As rates decline, increased buyer interest reduces active inventory, as homes are snapped up faster, reflecting stronger market demand. NAR data indicates that single-family home sales rose 1.1% year-over-year to an annual rate of 3.64 million in July, with median prices edging up just 0.3% to $428,500, nearly flat compared to broader home-price growth. In Miami, this translates to increased inquiries for waterfront and luxury single-family properties, as seen in rising mortgage applications for new builds, alongside a noticeable contraction in inventory levels as buyers capitalize on improved affordability. However, demand remains tempered: homes lingered on the market for 28 days in July, up from 24 days a year prior, per NAR. Our Miami Market Insight Framework quantifies this rate-demand-inventory link, showing that a 0.5% rate drop typically boosts single-family inquiries by 10-15% and reduces inventory by 5-8% in cyclical trends, based on historical Freddie Mac and local sales data.

LOOKING AT THE TRENDS IN THE MARKET

Examining the trends, mortgage rates’ dip to 6.58% aligns with a modest rebound in applications, but the Miami market’s slowdown is evident in permit declines and low sentiment scores. For instance, the NAHB index’s regional breakdown shows the South (including Miami) at a three-month average of 29, down one point and far below the national neutral of 50. This pattern suggests a cyclical trough, where high inventory, up 15.7% year-over-year to 1.55 million homes nationally, per NAR creates buyer leverage but fails to stimulate demand without rate relief.

If we reference a hypothetical chart of Miami’s single-family metrics (drawing from NAR and Florida Realtors data), it would illustrate permits trending downward since Q1 2025, contrasted with a slight uptick in sales volume post-rate stabilization. The key pattern: demand elasticity is high in this segment, with NAR noting that wage growth outpacing the 0.2% annual home-price rise positions buyers favorably for the first time in five years. Yet, without rates falling below 6.5% as suggested by Coldwell Banker Affiliates President Jason Waugh, acceleration in single-family demand may remain elusive, potentially extending the market’s lag into late 2025.

In summary, while mortgage rates at 6.58% offer a yearly low and some demand stimulus, Miami’s market slowdown, evidenced by low builder sentiment and tepid single-family activity, requires further rate reductions to fully ignite recovery. Data from NAR, Freddie Mac, and NAHB clearly indicate that inventory gains alone are insufficient; rate-driven affordability is the linchpin. Notably, a recent sharp increase in single-family permit activity signals that home builders are anticipating lower interest rates, which they expect will stimulate future demand, as permits serve as a leading indicator of builders’ confidence in market recovery. For Behind The Scenes investors, focus on monitoring single-family permits as a leading indicator within our Miami Market Insight Framework. Target properties in high-inventory areas like Edgewater or Brickell for potential appreciation if rates dip below 6.5% by year-end. This approach positions you to capitalize on emerging demand trends ahead of the curve.

ABOUT AUTHOR

Jaden Duxfield is a skilled Market Research Analyst at Sunland Group who brings a unique combination of strategic thinking and analytical expertise to the real estate industry. With a background in mechanical engineering and a degree from Auckland University of Technology, New Zealand, he offers a sharp understanding of the built environment. Jaden specializes in data-driven analysis to uncover emerging trends and guide investors and developers in making informed decisions. His proficiency in advanced statistics and Python programming is highlighted in his insightful blogs, where he transforms complex data into clear and actionable conclusions for industry professionals.

The information provided on this blog is for general informational purposes only and does not constitute financial, investment, or real estate advice. While I strive to present accurate and up-to-date information, the content may not reflect the latest market conditions or legal developments. Any reliance you place on such information is strictly at your own risk. Sunland Group and I do not make any representations or warranties regarding the accuracy, reliability, or completeness of the information provided.

Before making any financial or investment decisions, you should consult with a qualified professional who can provide advice tailored to your individual circumstances. Sunland Group and I will not be held liable for any losses or damages arising from the use of this blog or its content.

Blog

Explore our property blog for in-depth insights into residential and commercial market trends, lifestyle inspiration, expert advice and global real estate updates.

SUNLAND MARKET RESEARCH

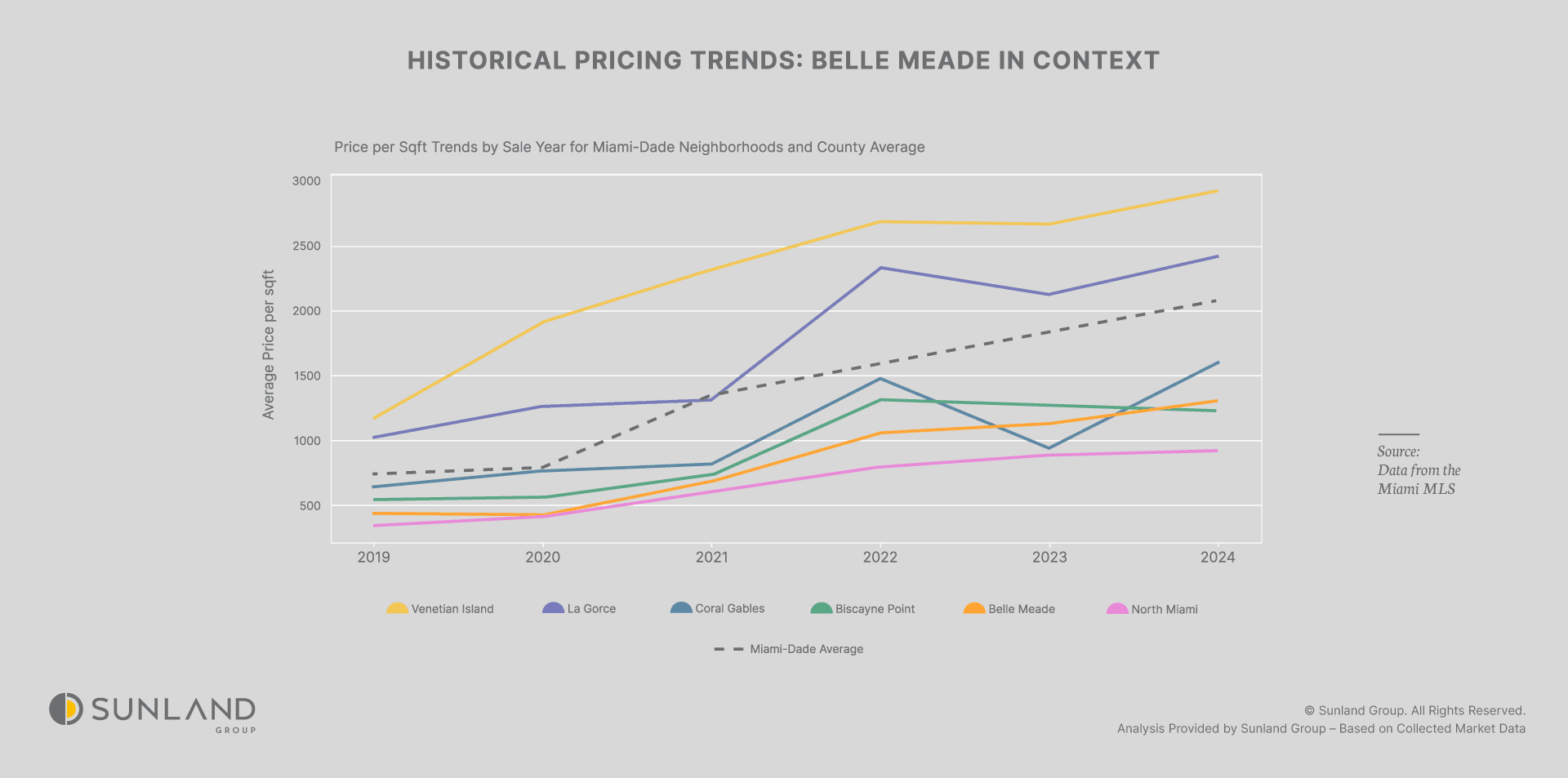

Positioning Belle Meade in Miami’s Exclusive Waterfront, Single-Family Housing Market

SUNLAND MARKET RESEARCH

Belle Meade Neighborhood Review

SUNLAND MARKET RESEARCH

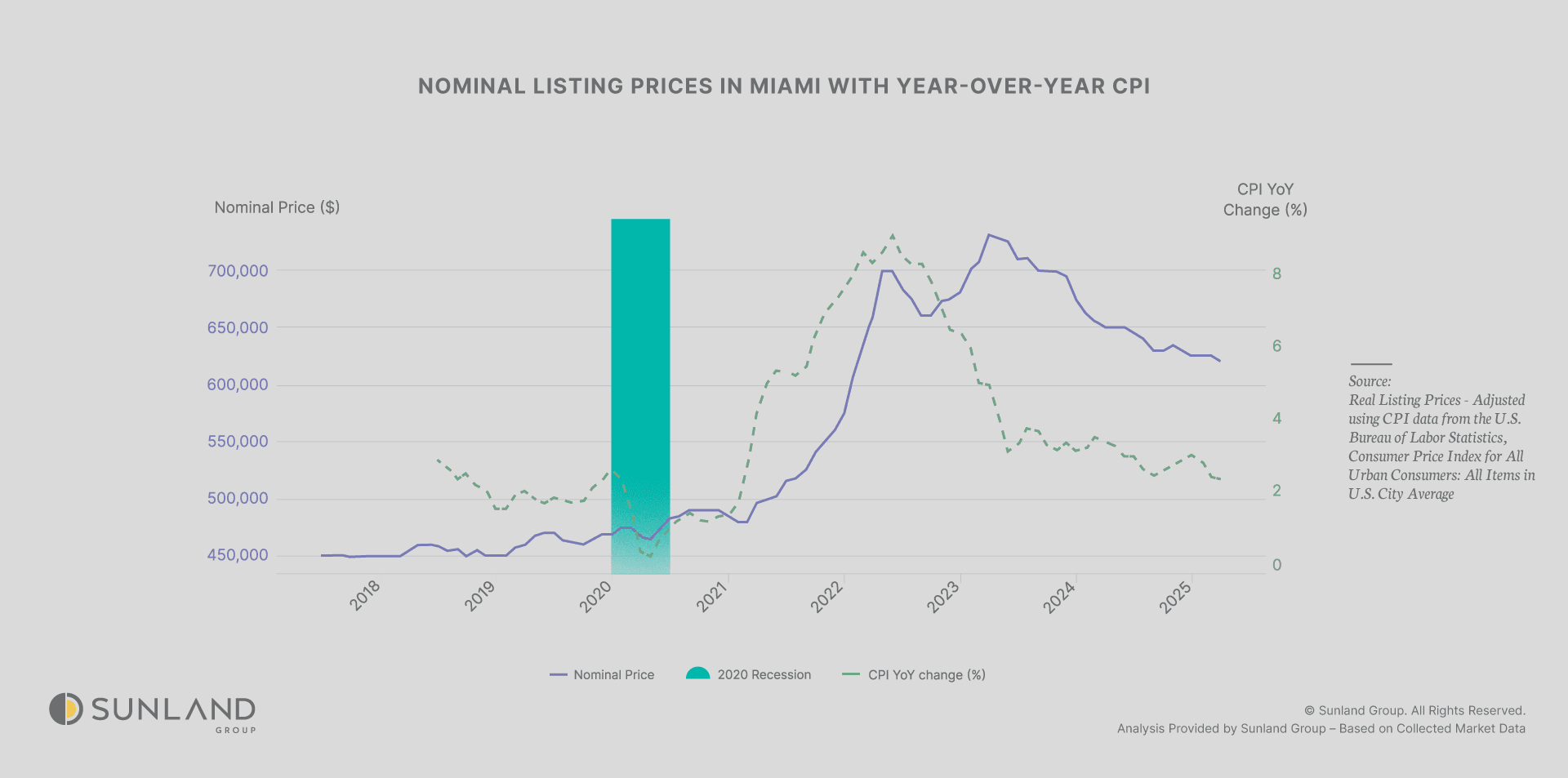

Real and Nominal Prices within Miami’s Real Estate Market

CORPORATE OFFICE

14 NE 1st Ave, Suite 305,

Miami FL 33132

PHONE NUMBER

(305) 209 1455